A key problem in improving Internet access has been ensuring residents and local businesses have high quality services. One means of ensuring high quality is via competition – if people can switch away from their Internet Service Provider, the ISP has an incentive to provide better services. However, the high cost of building networks is a barrier for new ISPs to enter the market - limiting the number of options for communities. Open access provides a solution: multiple providers sharing the same physical network.

Publicly owned, open access networks can create a vibrant and innovative market for telecommunications services. Municipalities build the physical infrastructure (fiber-optic lines, wireless access points, etc.) and independent Internet Service Providers (ISPs) operate in a competitive market using the same physical network. In this competitive marketplace, ISPs compete for customers and have incentives to innovate rather than simply locking out competitors with a de facto monopoly.

Open Access: An arrangement in which one network is open to independent service providers to offer services. In many cases, the network owner only sells wholesale access to the service providers who offer all retail services (ie: triple-play of Internet, phone, TV, as well as home alarm systems, and other types of services).

- See also "OK, Just What Does Open Access Mean Anymore" on how the definition is evolving.

- We may not agree with everything in this article at LightReading.com, but Debunking the Open Access Myths and the comments provide one of the most in-depth discussions on the topic.

The open access model is often compared to road systems. Roads are built and maintained through both public funds and taxes on vehicles, but do not themselves fill the coffers of municipalities. They are then used by everyone - trucking companies, UPS, taxi cabs, pizza delivery people, etc. - to deliver services or get around. For the municipality, the net gain of building robust road systems comes in economic development successes, improvements in quality of life, and other indirect benefits rather than direct profits.

Building open access broadband networks along the same principles has proven immensely successful at fostering competition and producing economic gains in some U.S. communities, but also more extensively in Sweden, France, and Japan. In the United States, this model has been used less frequently, in part because of differences in national regulation and the power of the largest corporations to shape policy.

Stockholm, Sweden, has one of the world’s most advanced open access networks. Its Stokab dark fiber network covers 90 percent of the city’s homes and business. Photo of Stockholm courtesy of Edward Stojakovic through Flickr Creative Commons

"At the end of the day, if a company wants a connection through our network, using a provider, they can get that at a price point that makes sense, and it's competitive." - Tad Deriso, President and CEO of the Mid-Atlantic Broadband Communities Corporation

In the United States, local governments that have their own community networks often own, operate, AND provide services on those networks. In a number of cases, local governments prefer to offer services directly because they can ensure a high quality experience. But many communities would rather not directly provide services because they don’t want to have to compete against powerful entrenched firms like the cable and telephone companies. Though the big cable and telephone companies could allow others to use their networks, they prefer to operate as monopolies.

Open access tends to be more common in middle-mile networks, which can connect large enterprises, than in last mile networks, which connect residents. Many ISPs are used to using middle mile networks that they do not control to connect their various last mile networks. Even large companies like AT&T lease connections from other providers in some cases.

Some private companies own and operate open access networks, such as CityLink Fiber in Albuquerque. However, other companies like CenturyLink and AT&T have long undermined any effort to require network owners to share their network infrastructure (even when it was paid for by the public under a regulated monopoly). When it comes to private companies building open access networks, we are supportive but fear the company could change its mind or be bought by a larger company with a different agenda. CityLink has written open access into its franchise agreement to guard against these concerns.

"We don't have to have the personnel to do that. We don't have to manage that infrastructure, and get all those calls for services. And having the private business do what they do best made sense." - Kim Kleppe, Information Systems Director of Mount Vernon

Open access networks spur competition between service providers - lowering both the costs for subscribers and the barriers to new service providers entering the market. They facilitate economic development, as new firms look to relocate to areas with more choices for reliable, high-speed Internet access and existing businesses can be better served.

But perhaps most importantly, the benefits of publicly owned open access networks are that the community enables innovation, ensures real choices, and has a strong voice over its own future. Below, we discuss some of the key benefits and challenges of this model. Additionally, we list networks where the model is in practice today.

Open Access Arrangements

Two-layer: In a two-layer arrangement, the municipality owns and operates the network (constructs and maintains the network, making sure everything runs smoothly). Services are distributed by ISPs.

- E.g. nDanville, Virginia

Three-layer: In the three-layer model, the municipality builds and owns the network, an independent party operates the network, and service providers bring fiber directly into homes and businesses.

- E.g. Rio Blanco County, Colorado

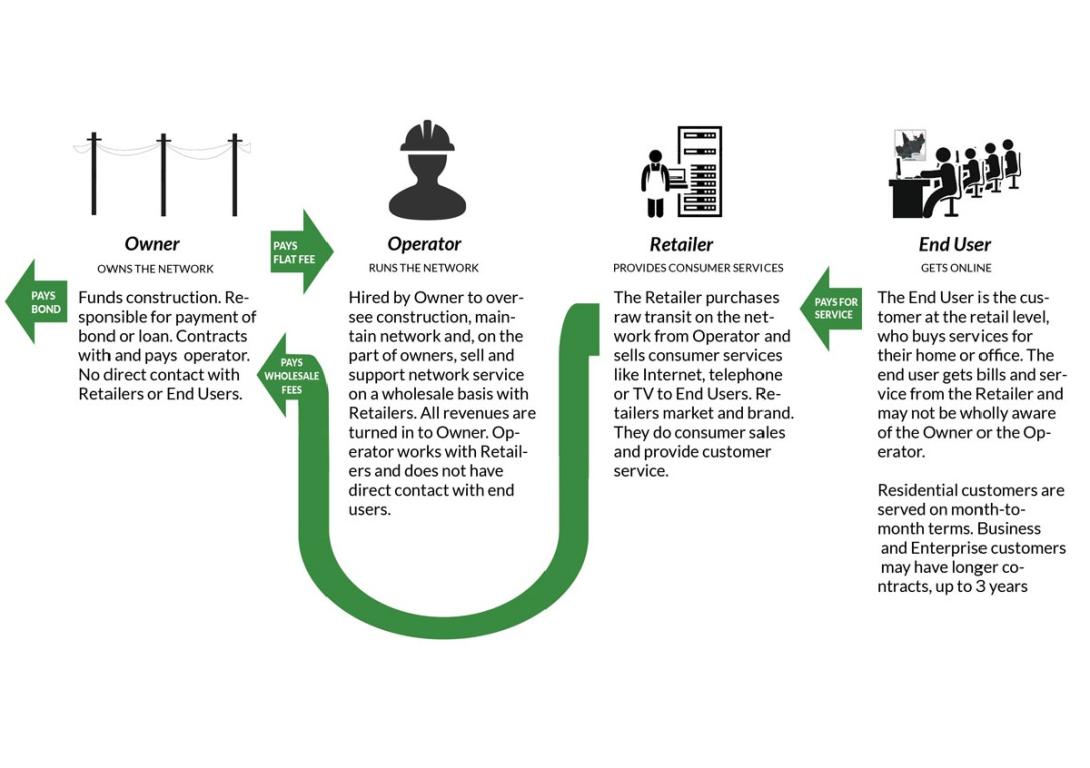

Below is an example of an open access arrangement. The network owner funds the construction; the operator oversees construction and maintenance. The retailers provide the Internet service required by us, the end users, who likely just want to get online to get informed, play games, and do work.

Infographic from Peggy Dolgenos, Cruzio Internet

Middle mile Open Access Network: The middle mile is the section of a network that connects local, last mile networks to the backbone of the Internet. Middle mile networks can cut across state boundaries and are able to transport large quantities of bandwidth between network endpoints. These networks may also connect towers (often for wireless services), community anchor institutions, and other large customers. Large firms like Verizon and Frontier have been known to sometimes lease middle mile circuits although they steadfastly refuse to use open access last mile networks.

- E.g. The Three Ring Binder in Maine, Mid-Atlantic Broadband in Virginia, NoaNet in Washington

Last mile Open Access Network: The last mile is the connection between the service provider and the home subscriber. On this type of network, home subscribers will have the option among multiple independent service providers delivering Internet access, telephone services, television, and potentially other services (burglar alarms, etc.). Many of these network in the United States start by serving businesses and then expand to residents incrementally.

- E.g. Palm Coast Fiber in Florida, Mount Vernon Fiber Optics and Chelan County Public Utility District in Washington

Dark Fiber Open Access Network: Dark fiber is laid but not lit during fiber buildouts, and left as unused capacity until needed or desired. The act of attaching the fiber to the lasers that send bursts of information across it is called "lighting" it. This type of network is inherently open access, as any provider could lease it (often with an agreement called an IRU, Indefeasible Right to Use). However, only large firms, very technical firms, and ISPs tend to be interested in leasing dark fiber.

- E.g. Axcess Ontario and Southern Tier Network in New York, Palo Alto Utilities in California

Financing Open Access Networks

Some, like Rio Blanco County have taken advantage of state grants to subsidize their network build-out. Rio Blanco received $2 million in matched funds from the Colorado Department of Local Affairs. It then committed another $7 million of its own funds to the project, made up of $2 million in federal mineral lease revenues and $5 million from the county's general fund.

With increasing federal emphasis on broadband, government funding for municipal projects might more often subsidize infrastructure investments in both lit and dark fiber networks. That said, communities have a number of tools at their disposal to fund these networks without federal money.

In New York, one community that was wary of relying on federal funding found another way to cover startup costs for its dark fiber open access network, Axcess Ontario. They tapped into a municipal economic development branch - the Ontario County Office of Economic Development/Industrial Development Agency. The network is now run as a non-profit, with a board of 12, but no paid employees. Revenues from businesses that want to use the network services pay the operation, maintenance, and debt costs.

Many communities, like Palm Coast, Florida, have opted for a phased approach to build their open-access infrastructure. Palm Coast FiberNET relies on a capital projects fund - a way of managing financial resources to complete large-scale infrastructure projects like highways. In building Palm Coast FiberNet, the City drafted a 5-year plan that split the $2.5 million infrastructure cost into five investments of $500,000. It connected community anchor institutions and government offices at the same time as it connected local businesses. The public savings from ending previous contracts with Comcast offset construction costs.

Another approach is to use Tax Increment Financing (TIF), a tool that allows specified districts to borrow funds for redevelopment that are to be paid back in future taxes, to subsidize infrastructural costs. TIF has aided in Bozeman, Montana’s effort to bring next-generation technology to their community.

Some networks place more of the financial responsibility on the network subscribers. In the utility fee model, subscribers (or all community members, depending on the arrangement) pay a monthly surcharge, which helps to fund the construction and maintenance of the network. A version of this approach is being used in Ammon, Idaho, which has two fees. The first is for the fixed cost of building it, and the second is for operation and maintenance. This last fee varies based on the total number of network subscribers: the more subscribers to the network, the less the individual cost.

Other networks use a wholesale model, selling bandwidth in bulk to ISPs, which can then be bundled, often in a triple-play (phone, TV, Internet) arrangement, and sold to customers. ISPs pay for the ability to provide services over the shared network. For example, Mount Vernon, Washington receives 15 percent of the gross income of each ISP that uses its network. In other cases, ISPs pay a one-time connectivity fee to be able to use wholesale services.

In some cases, communities have built their networks with the assistance of federal loans/grants along with community and private sector contributions. Fast Roads in New Hampshire is one example of this. Fed up with poor service in western New Hampshire, a coalition of municipalities built the Fast Roads network using a combination of stimulus funds from the American Recovery and Reinvestment Act (ARRA), community contributions, and private donations.

Even with these many options for financing, building a citywide network immediately is challenging. Many community networks start out incrementally. The revenue or savings from one section pays for the construction of the next section. Most begin by connecting community anchor institutions before moving on to connect businesses and residents. The public savings from ending contracts with incumbent ISPs enables communities to fund the expansion of the network, such as with Santa Monica, California’s City Net. Incremental financing works, especially in cities without a public power utility.

Challenges for Open Access Networks

While many municipal networks face challenges from incumbent providers and state laws, open access networks encounter a unique set of problems. The most obvious being, how to attract service providers to the network? After that, it then becomes a matter of maintaining the reputation of the network. In the long term, however, there may develop concern over price competition and consolidation. This section aims to provide solutions and advice for these open access problems.

Challenge 1: Getting Service Providers

There’s not much use in an open access network without service providers offering a variety of competitive services. In order to ensure the network’s success, there should be at least one core provider at the start. Some community networks begin with an operator who also acts as an ISP. For a set period of time, the operator will be the sole ISP before opening up the network to other ISPs. Westminster, Maryland, pioneered this model when they built a community network with the ISP Ting.

It may take time for ISPs to join the network. While incumbent ISPs do not often want to do business on the public open access infrastructure, other smaller, local ISPs may join. Some communities hire a specific person, such as the network director, to recruit service providers. Others wait for the reputation of the network’s speed and reliability to entice ISPS to the new market.

Challenge 2: Reputation

After securing service providers, the community faces a new challenge, building and maintaining the reputation of the open access network. In extreme cases where an ISP acts in bad faith, a network’s reputation will become so maligned that it struggles to rebuild its brand and attract new, better ISPs.

For example, Provo, Utah is often cited as proof of the failure of municipal networks. The network’s wholesale model (mandated by the state) relied on private ISPs that overpromised, under-delivered, and bowed out of the market too quickly. Provo’s network reputation was severely compromised.

Challenge 3: Price Competition and Consolidation

Some fear that in the long term ISPs will consolidate, leaving us once again with a duopoly or monopoly. These fears have yet to be realized, but it has become more of a topic in Sweden where open access networks have been in existence longer.

Over time, if the only differentiation between service providers is price, then eventually those profits will be competed away. Eventually people will choose the cheapest plan that suits their needs, and the ISPs will have to consolidate. This will diminish the number of options for the consumer – leading to the situation that open access meant to avoid all along. ISPs will have to take care to differentiate their services, preferably by competing for providing the most friendly customer support, in order to stay competitive and in business.

U.S. Open Access Networks

ILSR is currently tracking more than 30 open access networks across the United States.

Last Mile Networks:

| Name | Community Served | ISPs | Subscribers |

| Ammon Fiber Optic Utility | Ammon, ID | 2 | No available data |

| Ashland Fiber Network** | Ashland, OR | 4 | 4,200 Internet subscribers; 1,800 cable television (Data from 2010) |

| Benton PUD* | Benton County, WA | 5 | No available data |

| Bozeman Fiber | Bozeman, MT | 5 | No available data. Only serves business subscribers. |

| Chelan PUD* | Chelan County, WA | 11 | Offers access to 70% of 70,000 person county ~50,000 potential; 5,700 confirmed end users (Data from 2007) |

| Clallam PUD* | Clallam County, WA | 6 | No available data |

| Click! Network** | Tacoma, WA | 3 | No available data |

| Cortez Community Network | Cortez, CO | 7 | 250 businesses (Data from 2014) |

| Douglas County Community Network* | Douglas County, WA | 6 | Offers access to 45% of 15,000 person county ~6,900 (Data from 2013) |

| Eastern Shore of Virginia Broadband Authority* | Accomack and Northampton Counties, VA | 6 | 20-25% of Eastern Shore residences along existing fiber lines (Data from 2018) |

| EUGNet* | Eugene, OR | 6 | 32 connected buildings, 62 total signed up (Data from 2018) |

| FiberNET | Palm Coast, FL | 1 | 22 businesses (Data from 2011); 90% of 1,600 businesses in fiber range |

| Franklin PUD* | Franklin County, WA | 9 | Available to 68,000 customers (2015) |

| Grant PUD* | Grant County, WA | 16 | 16,000 subscribers (2017) |

| Grays Harbor PUD* | Grays Harbor County, WA | 10 | No available data |

| Holland Utilities* | Holland, MI | 6 | 450 businesses (Data from 2018) |

| Jefferson PUD* | Jefferson County, WA | 8 | No available data |

| Kitsap PUD* | Kitsap County, WA | - | 186 Active Ethernet circuits (Data from 2015) |

| Mason PUD* | Mason County, WA | 5 | No available data |

| MetroNet Zing | South Bend, IN | 19 | More than 150 subscribers (Data from 2014) |

| Mount Vernon Fiber Optics | Mount Vernon, WA | 9 | 160 businesses, 65 government entities (Data from 2017) |

| nDanville | Danville, VA | 3 | 150 businesses; one residential community (Data from 2015) |

| Okanogan PUD* | Okanogan County, WA | 9 | No available data |

| Pacific PUD* | Pacific County, WA | 3 | No available data |

| Pend Oreille County Community Network System* | Pend Oreille County, WA | 11 | 1,345 business and residential connections (Data from 2015) |

| Rio Blanco County Broadband Project | Rangely and Meeker, Colorado | 2 | No available data |

| Roanoke Valley Broadband Authority | Roanoke and Salem, VA | - | No available data |

| The Wired Road | Grayson & Carroll counties, city of Galax, VA | 3 | 80 homes; multiple anchor institutions (Data from 2012) |

| UTOPIA Fiber | 15 Cities | 35 | 25,000 FTTH subscribers (2019) |

Middle-Mile Networks:

| Name | Community Served | ISPs | Subscribers |

| Columbia county Broadband Utility | Columbia County, Ga | 5 | 150 CAIs (Data from 2017) |

| Mass Broadband 123 | 120 Mass. Communities | 12 | More than 1,100 CAIs, with plans to connect 400,000 homes & businesses (Data from 2014) |

| Medina County Fiber Network | Medina County, OH | - | No available data |

| Mid Atlantic Broadband | Southern VA | 11 | Reaches 100% of regional businesses, industrial, and technology parks (Data from 2014) |

| NoaNet | Washington State | 61 | 260,000 last mile customers (Data from 2015) |

| OpenCape | Cape Cod, MA | - | 110 CAIs (Data from 2016) |

| Southern Tier Networks | Chemung, Schuyler, and Steuben Counties, NY | 5 | 260 miles dark fiber available open for lease (Data from 2015) |

| The Three Ring Binder | Maine | 9 | 24 middle-mile customer agreements in place (Data from 2014) |

* PUD = Public Utility District. Because of Washington state barriers, PUDs are only allowed to sell wholesale broadband services. They are not allowed to retail services directly to customers, so they employ an open access approach. 9 PUDs are part of the statewide open-access network NoaNet.

** Hybrid Fiber-Coax (HFC) Networks, not FTTH

Planned Open Access Networks

(Data from 2016)

| Community | Details |

| Dakota County, Minnesota | Open access part of long term strategy |

| Ellsworth, Maine | $28,000 in tax increment financing; 5 potential ISPs |

| Hudson, Ohio | City conducted residential and business survey; approved contract with consultant for design + implementation |

| Missoula, Montana | Local business survey; identification of ISPs |

| Sanford, Maine | Partnered with GWI; received a grant from the U.S. Economic Development Administration |

| Westminster, Maryland | Partnered with Ting (initial period of exclusivity); built network |

Additional resources

Ammon's Model: The Virtual End of Cable Monopolies

The city of Ammon, Idaho is building the Internet network of the future. Households and businesses can instantly change Internet service providers using a specially-designed innovative portal. This short 20 minute video highlights how the network is saving money, creating competition for broadband services, and creating powerful new public safety applications.

Connect This! Episode 4 - Open Access Networks

- Berkman Center, Yochai Benkler: "Next Generation Connectivity: A Review of Broadband Internet Transitions From Around the World"

- Broadband Communities: “The Role of the Local Transport Provider”

- Broadband Communities: “Building a Nationwide Open Access Network”

- Broadband Communities: “Services are Key to Open Access”

- Community Broadband Networks: “The Challenge of Open Access: Lessons Learned”

- Design Nine, Andrew Cohill: "Broadband for America: The Third Way"

- Diffraction Analysis, Benoit Felton: "Stockholm’s Stokab: A Blueprint for Ubiquitous Fiber Connectivity?"

- Huffington Post, Bruce Kushnick: "Fast Lane, Slow Lane - No Lane - End Game in Telecommunications"

- ISE Magazine, “Incumbent Broadband Providers Versus Muni Broadband”

- OECD, “Stimulating Competition Through Open Access Networks”

- Community Broadband Bits Podcast

- Episode 3: UTOPIA and XMission

- Episode 85: Fork in the Road for Utopia: Forward or Backward

- Episode 86: How Ammon, Idaho Builds Digital Roads

- Episode 112: Missoula Pursues Open Access Fiber for Jobs

- Episode 128: Open Access and Incumbent Challenges

- Episode 159: NoaNet Touches Every County in Washington State

- Episode 164: More Details on the Northwest Open Access Network

- Episode 166: Danville's Incremental Strategy Pays Off

- Episode 172: Open Access Engineering Options

- Episode 173: Muni Fiber in Idaho Helps 911 Dispatch and First Responders

- Episode 176: Maine Model for Muni Fiber - Dark and Open

- Episode 177: Self-Financed EC Fiber Continues to Grow

- Episode 179: Local Internet Improvement Districts in New Hampshire

- Episode 180: Maine House Representative Pushes for Better Internet Access

- Episode 191: Exploring the Huntsville Fiber Model

- Episode 206: Glenwood Springs Shares Lessons Learned

- Episode 207: Ammon's Network of the Future

- Episode 208: CityLink Telecommunications in Albuquerque Prefers Open Access

- Episode 215: Open Cape Works With Communities for Last Mile

- Episode 221: Virginia's Roanoke Valley Opens Fiber Access

- Episode 223: Update on Utah's Open Access UTOPIA

- Episode 233: Bozeman Unique Fiber Model Gets Good Start

- Episode 237: Kitsap Residents Demand Fiber

- Episode 259: Ammon Examines Muni Fiber Impact

- Episode 269: Holland's Muni Fiber Pilot Expands in Michigan

- Episode 274: Mason PUD 3 Responds to Muni Fiber Demand with Fiberhoods

- Episode 279: Lessons From the Nation's Oldest Open Access Fiber Network

- Episode 294: Virginia's Eastern Shore Broadband Authority Steadily Expands Fiber Network

- Episode 316: Mason County PUD 3 Uses Innovation for Strategic Deployment

- Episode 320: Neighbors Investing Through Neighborly

- Episode 331: UTOPIA Is Not An Unreachable Dream, It's A Network

- Episode 337: Predictions for 2019, Year in Review for 2018

- Episode 338: Taking Control Through Software Defined Networks

- Episode 360: SiFi Speaks on Fullerton Open Access Project

- Episode 361: 5G Absurdity, Ammon Affordability, Speed Realities, and USF Caps

- Episode 386: Medina County Fiber Network and Lit Communities Reach for Ohio Residents

- Episode 388: Predictions for 2020, Reviewing 2019

- Episode 390: Collaboration Across the State Line, Idaho Falls and UTOPIA Fiber

- Episode 424: Is Open Access the Future?

- Episode 439: Organizing for Change in Kaysville, Utah